31 Dec 2025

|

Paul Godfrey

|

A Look Back at 2025

Tags:

Insight

Banking

Stay connected with us

Keep up to date with Goodwood across our social channels.

Reflecting on the year, we have seen a few patterns that stood out across the clients we worked with and the banks they were dealing with.

Client insights

Some consistent themes came up in client conversations and their P&Ls during 2025 were:

Rising rents and occupancy costs became a significant cost increase for many businesses, often more material than funding costs themselves.

Topline growth was more modest, though this was somewhat offset by slower wage growth which helped stabilise margins in a number of sectors

There was a clear return to pre-COVID dynamics, where performance was more closely linked to business acumen and decision-making, rather than external tailwinds or luck.

Many businesses were in a better position to renegotiate fixed costs (freight, electricity, and insurance). Particularly those that had taken a disciplined approach in prior years.

Bank insights

From a banking perspective:

Banks became increasingly specialised, with fewer trying to be all things to all borrowers. Individually, each had clear strengths and weaknesses, but taken together they were able to cover the market well when deals were placed appropriately.

Credit appetite remained reasonably strong, and approvals themselves were generally achievable. The challenge was less about access to capital and more about structure and fit.

In most cases, the additional premium charged by non-banks wasn’t worth it unless there was a genuine structural reason to be there. Where a deal could be shaped to fit bank parameters, the long-term outcome was usually better.

High banker turnover continued to be an issue, with clients being introduced to new relationship managers far too often, making continuity and long-term context harder to maintain.

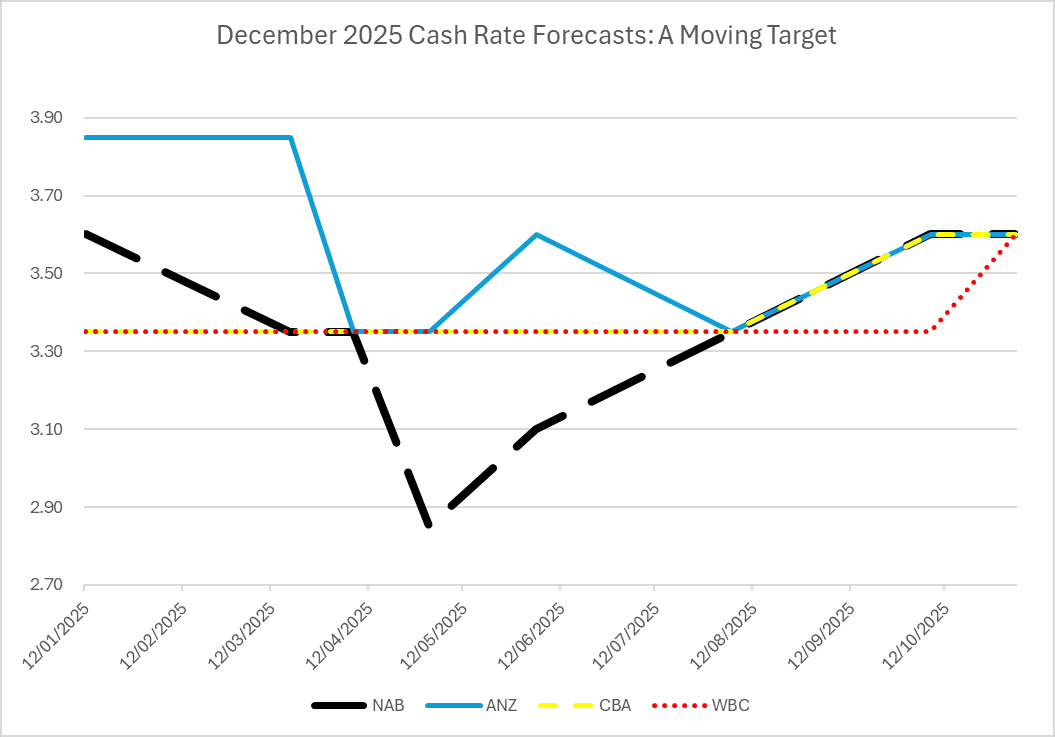

Cash rate expectations moved almost as often as the commentary around them. The chart below shows what each of the major banks thought the cash rate would be in December 2025, at different points during the year. It was a useful reminder that even the best resourced economists have no idea which way (and when) the cash rate will move to next

The core theme was that businesses with a clear understanding of their cost base, long term plans, and funding structures were generally better placed to navigate the year. It proved a better strategy for business owners to ignore the market noise and instead focus on what they do best - their core offering.